Author: Elisa Dell’Apa

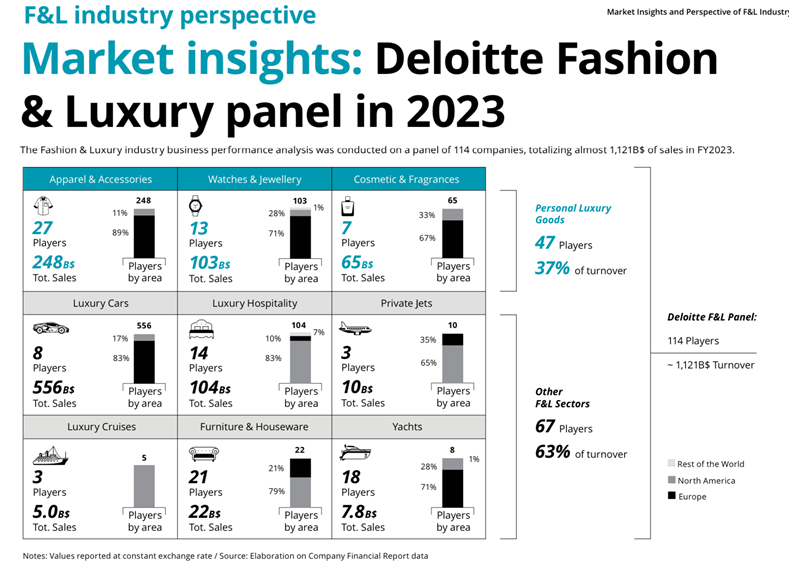

In September 2024 Deloitte presented in Milan its report “Fashion and Luxury Private Equity and Investors Survey 2024”, a study globally conducted with a panel of 114 companies that operate in Apparel & Accessories, Watches & Jewelry, Cosmetics & Fragrances, Luxury cars, Private jets, Cruises, Furniture & Houseware and Yachts.

A brief overview

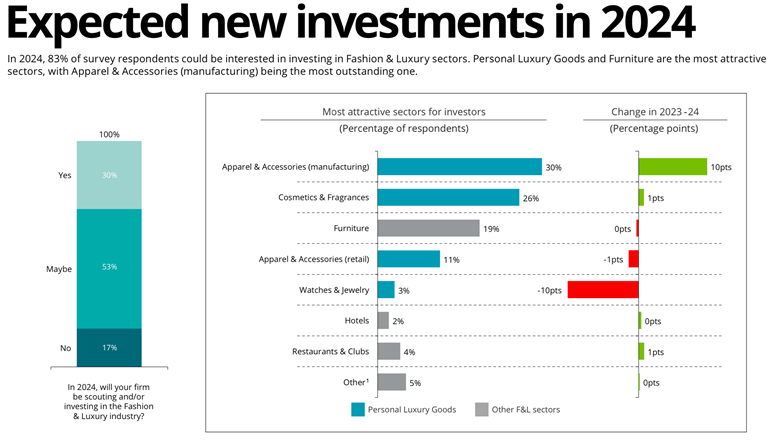

First of all, the survey confirms how, despite the complicated current geopolitical situation (decline of the Chinese market, macroeconomic uncertainty, international conflicts and wars) the Fashion and Luxury industry keeps attracting investors at a global level: 83% of interviewed investors is considering investing in Fashion and Luxury, with the highest sectors being Apparel & Accessories (30%), Cosmetics & Fragrances (26%), Furniture & Houseware (19%) and Retail sales (11%). Interestingly, more than 50% of the investors were mainly interested in consolidating small and medium companies rather than big ones.

Expected trends

Despite the general step back, China is going to become the biggest luxury market in the world, with almost 25% of purchases by 2030. Moreover, many companies are investing to become more and more attractive to young generations, since generations Y, Z and Alpha will account for 85% of purchases by 2030. By the same year, single-brand stores and e-commerce will be the main channels of luxury purchases with almost 60% of market share. To sustain the future growth companies are investing in solid technological infrastructures and focusing on pricing strategies based on exclusivity, product scarcity and the concept of limited editions. Finally, the luxury sector has been shifting towards quiet and experiential luxury: companies with the resources and the vision to craft iconic timeless pieces, service ecosystems and immersive experiences are thriving.

M&A agreements data

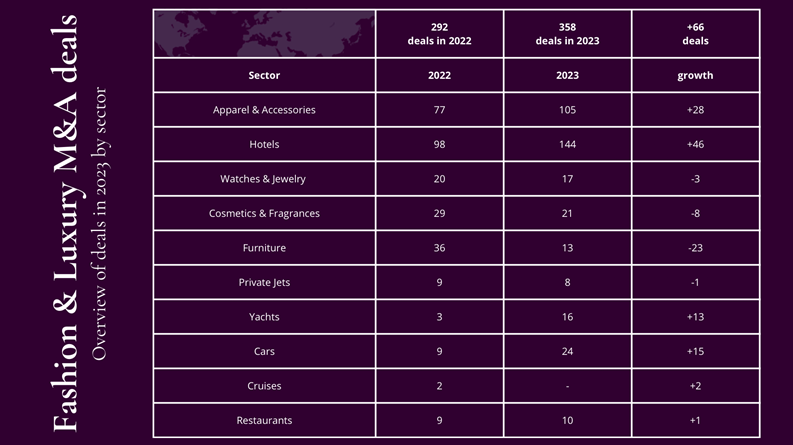

After a two-years-long slowdown, M&A operations have been significantly increasing. The most attractive sectors are Apparel & Accessories (30%), Cosmetics & Fragrances (26%) and Furniture (19%). As in 2023, also in 2024 the M&A market has been pulled by the sectors of Hotellerie (+ 46 deals VS 2022), Apparel & Accessories (+ 28 deals VS 2022), Cars (+ 15 deals VS 2022) and Yachts (+ 13 deals VS 2022). On the other hand, Furniture and Cosmetics & Fragrances have registered respectively -23 and -8 deals compared to 2022.

From a geographic point of view, Asia registered the highest growth (+ 30 deals VS 2022), followed by Europe (+ 17 deals VS 2022) and North America (+ 17 deals VS 2022).

Stable marginality

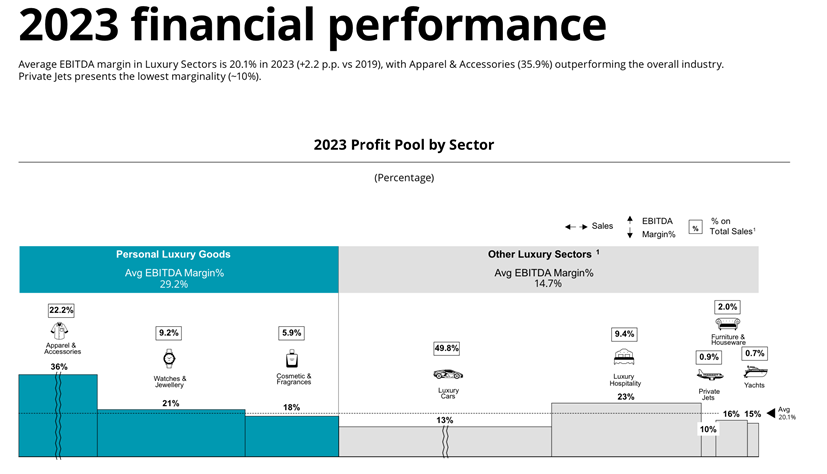

The overall marginality of the Fashion and Luxury sector has increased. The Personal Luxury Goods sector (which comprehends Apparel & Accessories, Watches & Jewelry and Cosmetics & Fragrances) was the highest performing one, gaining +2.7% of EBITDA margin compared to 2019, despite a slight decrease (-0.5%) compared to 2022. The other luxury sectors have registered a similar trend, with an increase of +0.3% in EBITDA margin compared to 2019 but a slight decrease (-0.2%) compared to 2022.

The average EBITDA margin has increased by +9.6% for the Personal Luxury Goods sector and by +12.0% for the other sectors. The overall average EBITDA margin in 2023 was 19.1% (+1.2% VS 2022): the highest margin was reached by the Apparel & Accessories sector (35.9%) while the lowest margin was touched by Private jets and Cars (between 10 and 13%).

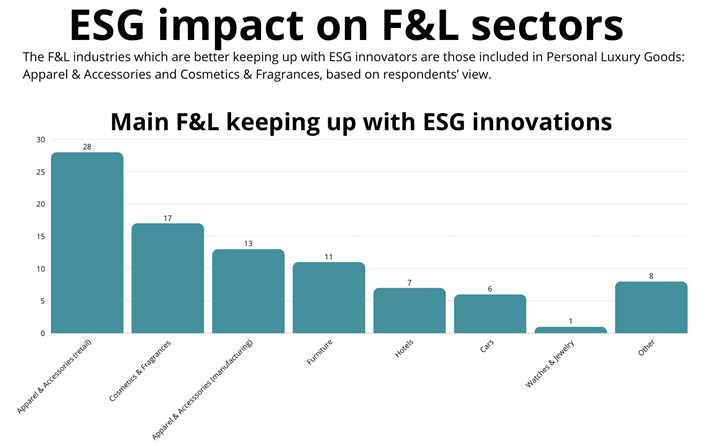

ESG and innovation

The Personal Luxury Goods sector is the one which keeps up the most with ESG innovations. 81% of the investors manifested their willingness to invest in new technologies, with a growth of 13% compared to 2023. With no doubt, artificial intelligence, big data and IoT will have the biggest impact on investors’ actions.