Author: Yağız Kökal

Abstract

This article will answer the question of “are we witnessing a sustainable transformation, like a transformation to electric, or a dangerous asset bubble like the dot-com bubble?” It will explore the five bubble metrics, discuss how normal the current situation is by providing market data, and recent investor moves.

Introduction: The largest tech companies are heavily investing in AI

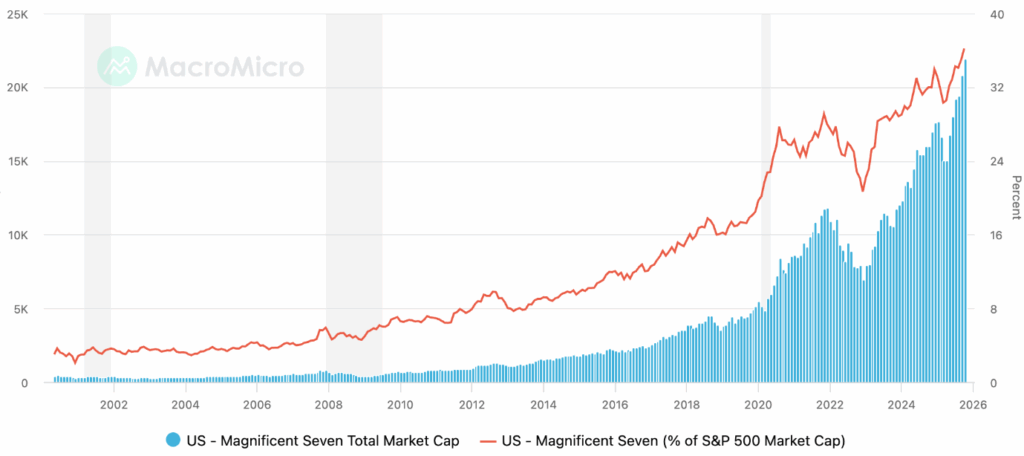

The size of this market is literally enormous; in the top 10 of the S&P 500, 8 of the companies are technology companies, and most of them are related to AI and the “magnificent seven” tech companies (Apple, Microsoft, Amazon, Alphabet, Meta, and Tesla) are there as well, having a total market cap of 21,924 billion and occupying 36.19% of the S&P 500 index.

These firms are already planning to pour $400 billion more into artificial intelligence by the end of this year. OpenAI’s CEO, Sam Altman, explicitly said, “Whether we burn $500 million a year or $5 billion—or $50 billion a year—I don’t care, I genuinely don’t,” he continued. “As long as we can figure out a way to pay the bills, we’re making the AGI (stands for artificial general intelligence, which is a hypothetical AI with human-like cognitive abilities). It’s going to be expensive.” These initiatives and huge market caps raise a lot of questions, but the most important one will be: Is this a new era of productivity and technology, or the peak of a financial cycle driven by hype and fear of missing out?

The Case for a Bubble

First phase of a bubble is displacement, where institutional and individual investors see a so-called “new paradigm”, which can be any new technology that seems promising or a sudden, powerful move from high-profile politicians (i.e., an interest rate cut or imposing tariffs from U.S. President Trump). In our case, this is artificial intelligence; it’s been seen as the new big thing that “we shouldn’t miss”. Secondly, there is the boom, when this happens, the prices rise slowly in the beginning, following a displacement; however, then as more people enter the market, this “boom” gets closer and closer. Fear-of-missing-out (FOMO), what could be a lifetime opportunity, attracts more speculation and uneducated investments, and money allocation. The third period is the “Euphoria”, during this phase, everything looks all sweet and perfect, but while investing, caution and educated investment decisions are thrown away as asset prices skyrocket. Everything reaches extreme levels. The fourth phase is the profit-taking period, where smart money (educated investments made by knowledgeable financial professionals) starts selling their positions, thinking that the “bubble” is going to explode soon. Finally, there is the “Panic” period, after the smart money started leaving the bubble, even a minor event can burst the bubble and once it’s burst, the bubble is not inflating again. For instance, the most commonly known example of this is the 2008 mortgage crisis, when Lehman Brothers declared bankruptcy (September 2008), the S&P 500 index lost almost 17% that month, and the systems (basically everything) collapsed, resulting in a huge regulatory and bankruptcy era in the housing market and banking in general.

Do we have the same periods on the AI market?

In short, not really. Dismissing the AI boom means dismissing the powerful, tangible forces to pay; the foundation is real and strong. The revenue is real and massive; this is the single biggest argument against a dot-com style bubble. In the dot-com era, companies went public with small or no foundation, no revenues, or no path to profit, hence, the bubble periods were super real. For instance, people had FOMO during that era and invested blindly in tech firms just because they had the “.com” top-level domain. On the other hand, in AI, these empty IPOs (initial public offering) don’t exist, or the companies out there are not small, and quite the opposite, they have super deep pockets. For example, arguably the most successful AI/Tech company Nvidia’s data center revenue exploded from $3 billion per quarter to $18 billion in just two short years. This isn’t just a speculative hope; it’s cash flow coming into the balance sheets. Unlike vague promises of the internet bubble, AI is already creating strong benefits. From 500 Fortune companies using AI to lower customer service costs by 30% to software developers using AI to cut development times by 50% and this is not a future promise; this is today’s reality.

However, this doesn’t mean that the AI hype is definitely normal and healthy

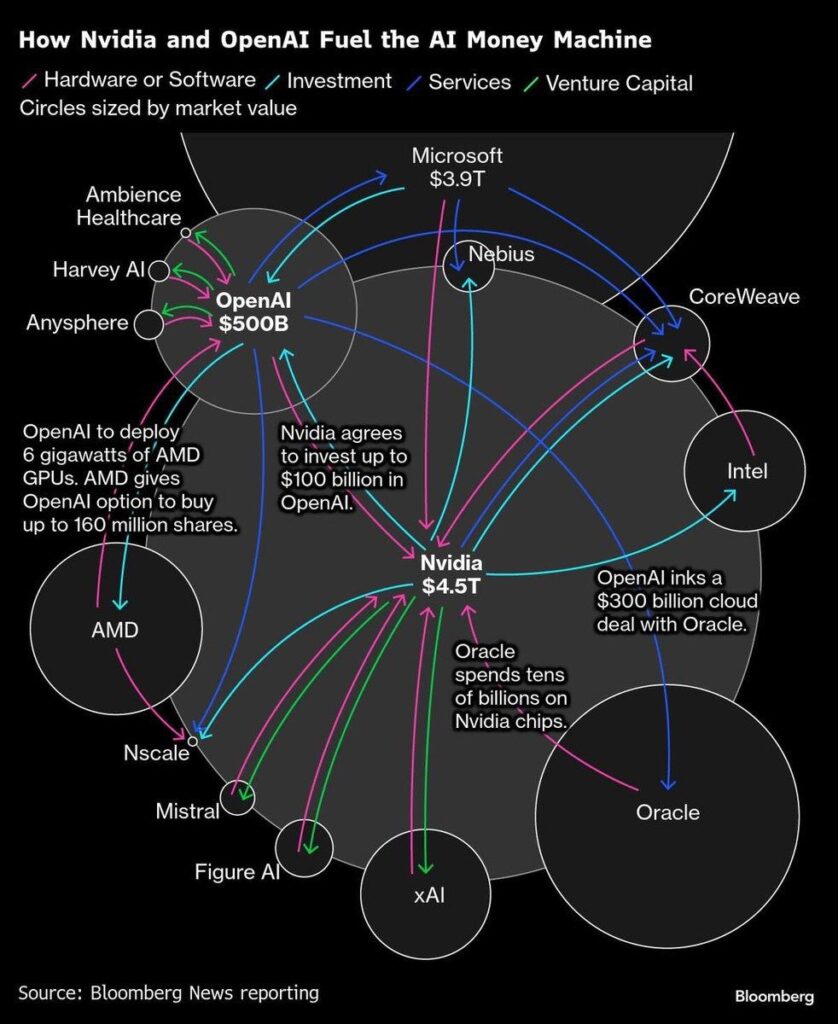

Beyond sky-high valuations, an interesting phenomenon is happening: a closed-loop financial ecosystem that some analysts fear is artificially inflating the AI sector, creating a web of circular investments and agreements between huge players, as the diagram below provides

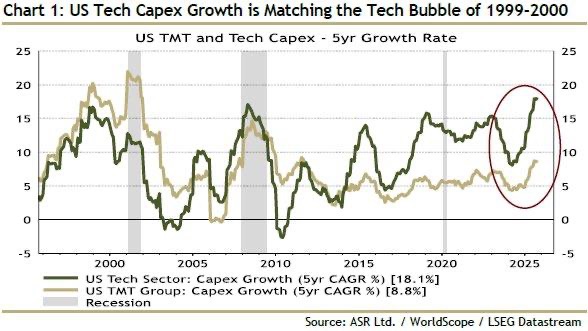

This creates a self-protecting cycle where capital and revenue circulate within a small group. The critical question about this is whether this is sustainable in the long run, and when it is going to expand to a broad, external customer base and the argument that we are in a bubble is not a total lie, it is supported by the data that comes from one of the most infamous periods in investing history. As the chart explains, the current 5-year growth rate in the U.S. Technology and TMT (telecom, media, and technology) capital expenditure has risen to a level that matches the peak of the late 90s dot-com bubble.

Overall, the debate over AI’s true value is not only academic; it has its spot in the real-time portfolio of one of the world’s most distinguished investors: Michael Burry, who correctly predicted and created profits of more than $700 million to his investors and $100 million to himself by predicting that the mortgage market was a huge bubble (2008 mortgage crisis). Just yesterday (4th of November 2025), his company, Scion Asset Management, disclosed that it has bought bearish financial products, called options, that will pay out if the price of AI-linked companies Nvidia and Palantir fall. Burry’s bets are controversial, Palantir’s CEO called the idea of shorting his company and Nvidia “crazy”.

Conclusion

There is no absolute answer to the question “Is the AI hype real or is it just a bubble that is about to explode?”. On one side, believers see limitless potential, profit, green graphs, and green bank accounts. On the other hand, skeptical thinkers like Burry see the classic patterns of overexcitement and vague pushes, where circular deals and hearsay-driven valuations move away from the economic reality of markets.

References

Barlevy, G. (2015). Bubbles and fools. Economic Perspectives, 39(2), 54-77.

Floridi, L. Why the AI Hype is Another Tech Bubble. Philos. Technol. 37, 128 (2024). https://doi.org/10.1007/s13347-024-00817-w

Rapley, J. (2024, February 24). Yes, artificial intelligence is fuelling a bubble, and it will eventually burst. Globe & Mail [Toronto, Canada], B2. https://link.gale.com/apps/doc/A783826311/AONE?u=anon~9c4b0623&sid=googleScholar&xid=cc93405b

Troy, S. (2025). Understanding the 5 Stages of an Economic Bubble

Meghan, B. (2025) Big Tech Is Spending More Than Ever on AI and It’s Still Not Enough

U.S. Magnificent Seven Total Market Cap & Share of S&P 500.

Christian, H. (2024). OpenAI’s Sam Altman doesn’t care how much AGI will cost: Even if he spends $50 billion a year, some breakthroughs for mankind are priceless.

William, S. (5 November 2025). Global stocks slip as US sell-off over AI valuations spreads.

Subrak, P. (Bloomberg Terminal), (2025, November 4). Burry Reveals Nvidia and Palantir Puts After Bubble Warning