The global financial landscape is currently witnessing a profound shift in how capital is deployed within critical infrastructures. In this evolving context, the water sector is no longer viewed as a stable utility niche, but as a strategic “Blue Gold” asset class. As we navigate 2025, the sector is redefining market boundaries, driven by a unique intersection of technological innovation, climate urgency, and appetite for resilient assets. To understand the current state of Water M&A sector, one must first analyze its volatile journey over the last 5 years, which is a masterclass story of record-breaking peaks, sharp corrections, and a sophisticated recovery.

The Parabola of Capital: 2021 to 2025

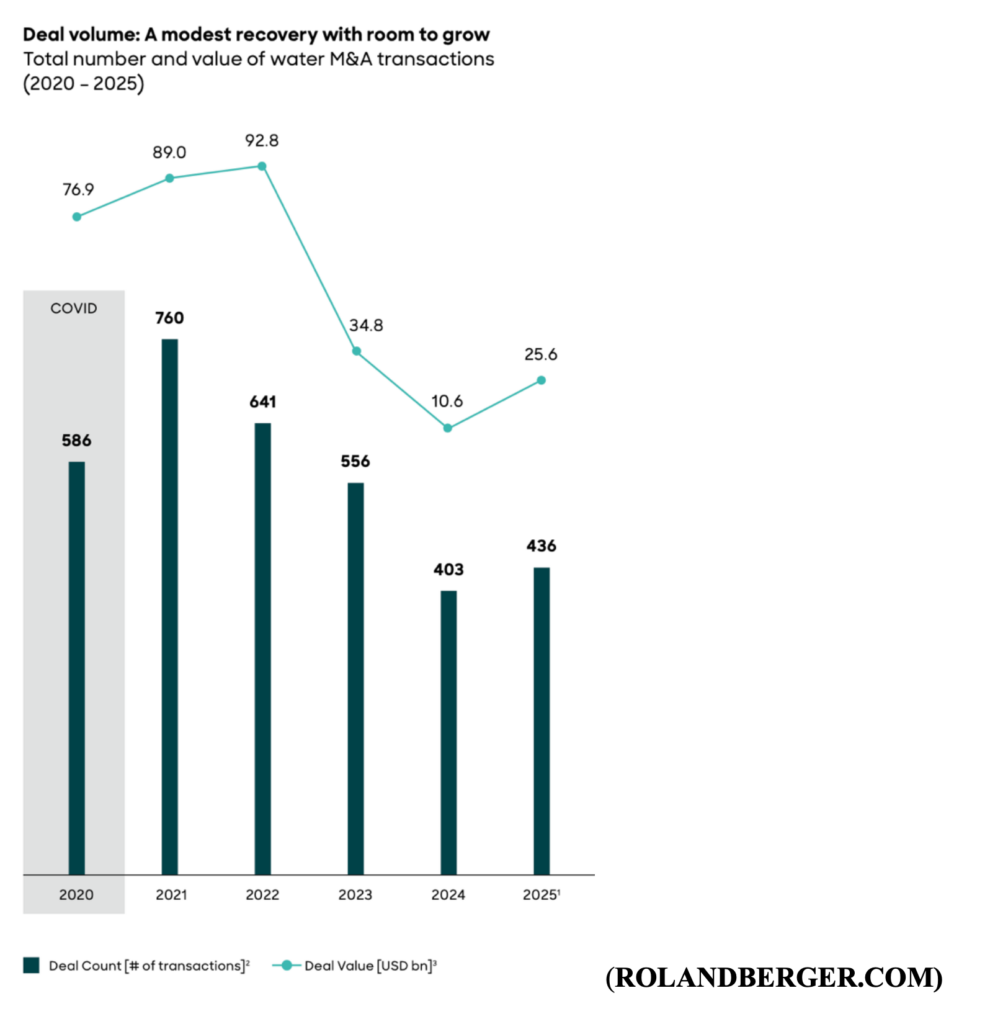

Starting from the post-pandemic period, 2021 saw an unprecedented 760 completed transactions with a total deal value of $92.8 billion, fueled by high liquidity and a global focus on infrastructure robustness: it was an era of “mega-deals” and rapid market consolidation.

However, the subsequent three years brought a necessary, despite painful, correction: from 2022 through 2024, the market entered a dropping phase. By 2024, transaction counts had fallen to 403, while disclosed deal values plummeted to $10.6 billion. This contraction reflects broader uncertainty among strategic buyers amid equity market volatility, weaker economic growth, and regulatory complexity, “prompting many established players to reevaluate timing and strategic focus in their inorganic growth plans” (Smart Water Magazine).

Entering 2025, the narrative has shifted once more towards a welcome reversal, with the market posting its first year-on-year growth in three years. Although the 436 deals completed in 2025 represent just 57% of the 2021 peak of 760 transactions, there was an 8% increase from 2024 resulting from investors’ renewed interest. The scale of recovery remains modest in terms of value, sitting at roughly $26 billion, but it also suggests something about the deal architecture: the 2025 scenario is driven by mid-market activity and strategic, technology-focused acquisitions rather than the mega-deals consolidations of the past (post-pandemic) period.

Several factors converged to support the rebound:

- Policy frameworks continued to act as boosters, with examples like the UK, where the AMP8 framework is expected to nearly double water utility investment over the next five years, and the United States, where the Infrastructure Investment and Jobs Act’s provided an authorization of approximately USD 50 billion in water infrastructure spending through 2026. However, regulatory environments remain subject to political shifts.

- Technology integration and digital transformation plays a pivotal role, with AI-driven water efficiency solutions leading to premium valuations. Several transactions were driven by implementation of predictive analytics, advanced sensors, and leakage detection technologies: major examples include Ecolab’s (a global company providing water, hygiene and industrial sustainability solutions) USD 1.8 billion acquisition of Ovivo’s Electronics business (a specialized provider of high-tech water treatment systems) and Veolia’s (a French multinational leader in water, waste and environmental services) acquisition of the remaining (30%) stake in its Water Technologies and Solutions business for approximately USD 1.75 billion.

- And lastly also the stabilization of interest rates (although elevated by historical standards) played a role, providing greater debt availability and financing clarity and predictability compared to the volatile conditions of 2023 and early 2024.

Geopolitics and the Brazilian Frontier

In this new environment, the “where” of investment is just as important as the “how. ” North America and Europe continue to account for nearly 90 % of total deal count, maintaining the geographical patterns that have characterized water M&A for years. However, while traditional Western markets have navigated a more cautious environment, with firms like Bluefield Research (a consultancy specializing in water industry analytics) reporting only 71 deals in the first half of 2025, other regions are becoming the true engines of growth.

Brazil stands out as a primary example of this evolution, deserving particular attention especially analyzing the country’s social situation: more than 33 million Brazilians still lack access to safe water, and 80 million live without sewage treatment. To address the water scarcity challenges, in 2020 Brazil approved the New Legal Framework for Sanitation, breaking the century-cycle of public-sector monopoly while opening the market to private participation (not without strict regulatory oversight).

The new Framework established different and ambitious goals to meet, including universal water access by 2033: from an investment point of view, this goal means that Brazil must double its current investment pace, deploying around BRL 550 billion (USD 105 billion) over the next 10 years. The introduction of the reform has attracted both domestic and international investors, as evidenced by the 150% surge in infrastructure M&A deals in 2024 compared to 2023, reported by Valor, allowing Brazil to position itself as a hub for “green water” solutions and utility management. Among the several significant water infrastructure projects there have been 3 over the past six months that deserve attention:

- Piauí concession: A 35-year full-service concession awarded to Aegea Saneamento for USD 175 million, with investment commitments exceeding USD 1.5 billion;

- Sergipe concession: A 35-year water and sewage services concession awarded to Iguá Saneamento for USD 815 million, with total commitments exceeding USD 1.1 billion;

- Pernambuco: A 35-year concession for water and sewerage services awarded to a BRK-Acciona consortium, involving approximately USD 2.8 billion in investments to serve roughly million people across 151 municipalities.

The Framework also increased private participation, which surged from 13% in 2012 to 42% in 2024, significantly improving shareholder value creation, as demonstrated by the case of one of Brazil’s largest water utility, Companhia de Saneamento Básico do Estado de São Paulo (Sabesp): following its partial privatization in July 2024, Sabesp reported a 171.9% annual increase in net income for 2024, reaching R$9.58 billion ($1.68 billion), alongside a 19% year-on-year rise in adjusted EBITDA to R$11.3 billion ($1.98 billion), according to Rio Times.

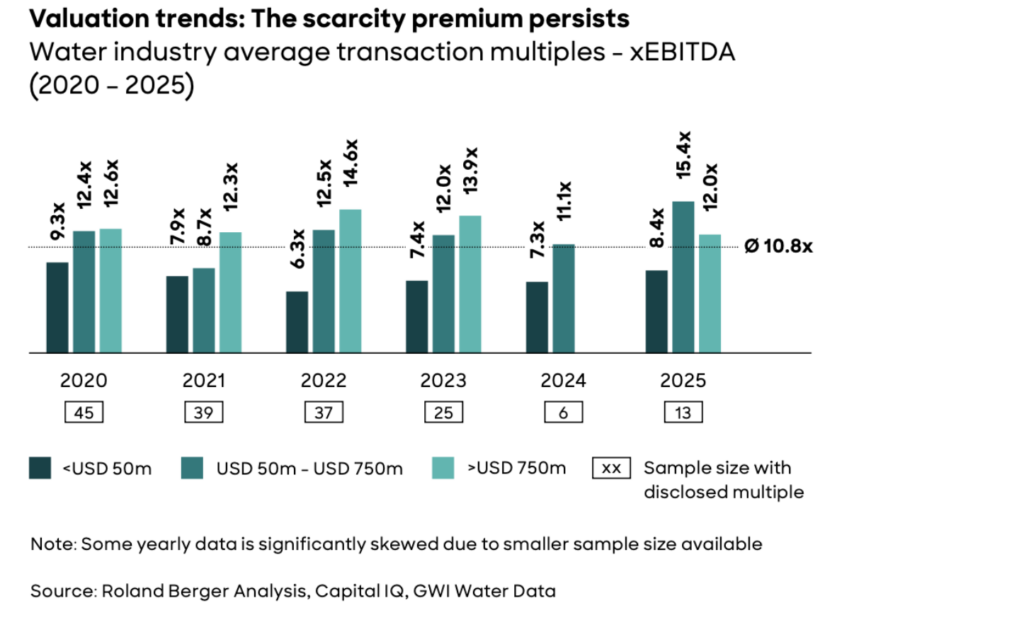

The ‘scarcity premium’ leading water valuations upwards

Water assets continued to trade at premium valuations in 2025, even though only a limited number of transactions disclosed full financial details. On average, deals were priced using a transaction multiple around 10.8x EBITDA, consistent with the presence of a “scarcity premium”: in other words, high-quality water infrastructure remains attractive because of its essential nature and the limited availability of investable assets in the sector.

Inevitably, the water market has become more competitive (it follows the rule of the “best-bid wins”): two transactions examples are the one of EQT’s (one of Europe’s largest private equity firms), which in the second half of 2025 acquired Seven Seas Water group (a leading provider of decentralized water and wastewater solutions), and of TAQA’s (major energy and infrastructure player from the Middle East), which acquired GS Inima (a major operator in desalination and wastewater treatment) as part of its strategy to grow internationally in desalination and wastewater treatment. Together, these examples show how water is no longer viewed only as a traditional utility sector, but as a strategic and competitive investment space where scarcity, innovation, and sustainability converge.

Long-term resilience horizons

The 2025 recovery in water M&A is a testament to the sector’s long-term resilience. The market is moving toward a more sophisticated phase that values technology-driven acquisitions, climate adaptation, and operational efficiency rather than scale-size.

Looking ahead, the “Blue Gold” narrative is likely to remain central. As climate challenges intensify and infrastructure needs expand globally, finance will play a key role in directing capital toward solutions thatgenerate both economic value and social impact. In this sense, the future of water M&A will not only be about valuations, but about shaping one of the most essential resources of the 21st century.