A cura di Gabriele Malloggi

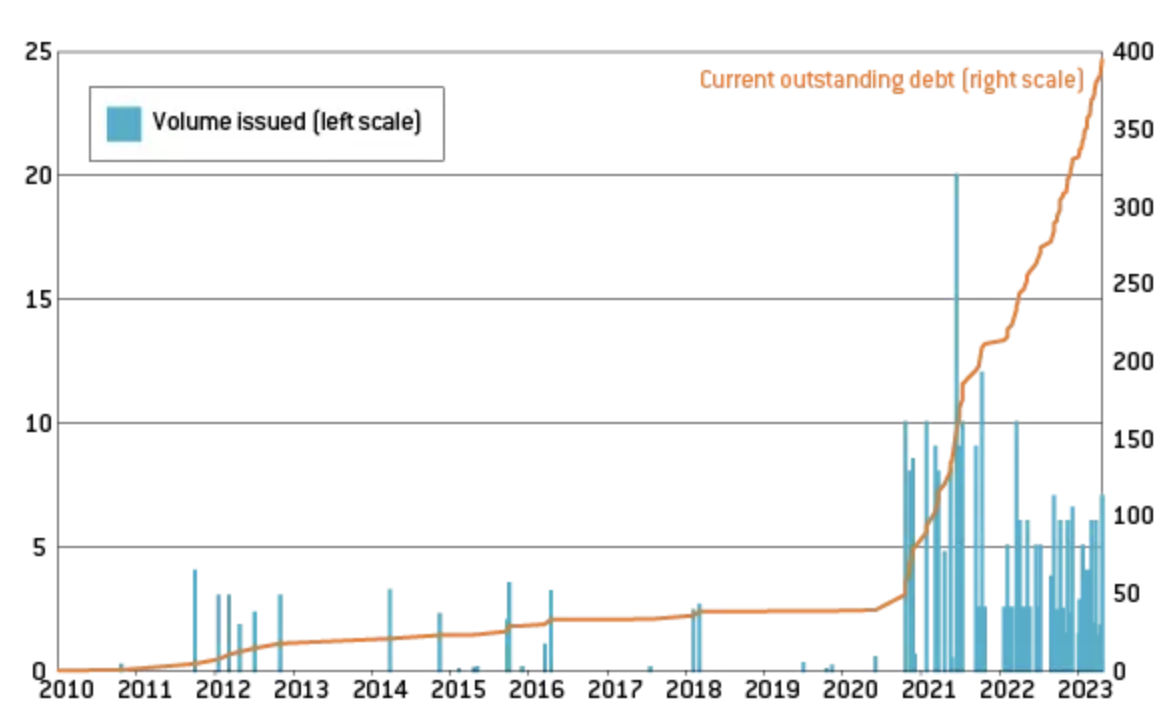

The EU is facing considerable investor skepticism due to the transformative impact of the COVID-19 pandemic on its borrowing practices. The introduction of unprecedentedly large and ambitious initiatives such as SURE and NextGenerationEU led to a dramatic shift, propelling the EU from a minor player in the sovereign market to a major one. In just two years, EU debt ballooned from approximately €50 billion to over €400 billion.

This development has been widely hailed as a significant political victory for the EU and a substantial leap forward in the integration process. However, recent price data indicating a rise in interest rates on EU-issued debt has sparked concerns about the long-term success of these collaborative borrowing programs.

EU debt issuance has surged to €450 billion and is expected to surpass €500 billion next year. This increase is primarily attributed to financing green initiatives, pandemic recovery endeavors, and assistance for Ukraine. Estimates suggest that by the end of net issuance in 2026, the overall size of this market is projected to exceed €1 trillion. This calculation includes the combined amounts from various programs: €50 billion carried over from previous initiatives, €100 billion for SURE, €750 billion for NGEU, and additional financial aid allocated to Ukraine.

Source: Bruegel based on Bloomberg and European Commission

And while the main issuers before the pandemic were the European Investment fund (EIB), the European Stability Mechanism (ESM) and the European Financial Stability Facility (EFSF), SURE bonds, NGEU bonds and Macro Financial Assistance (MFA) bonds are issued by the European Commission itself.

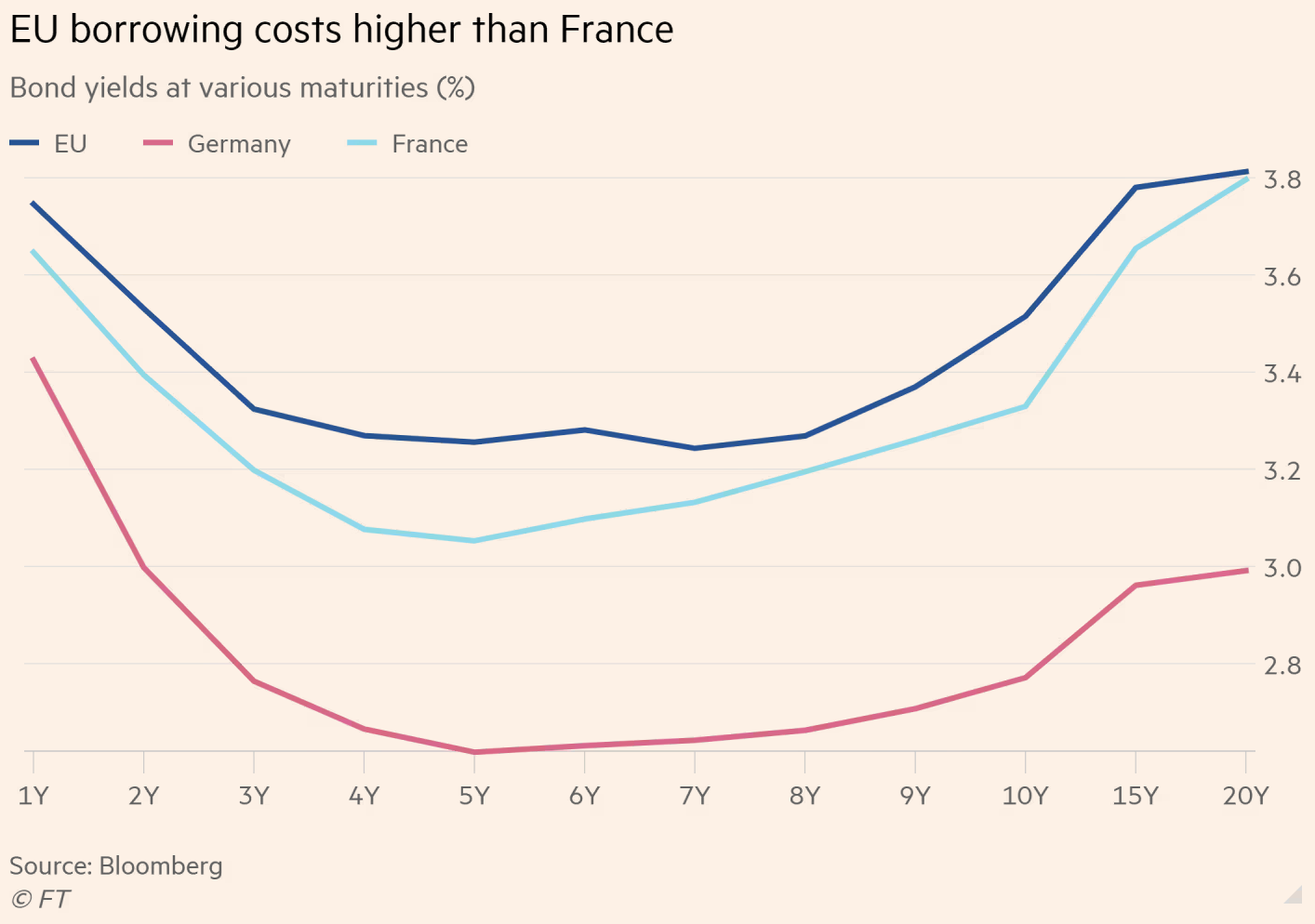

But despite the EU’s AAA credit rating, 10-year EU bonds command a 3.6 percent yield, in contrast to Germany’s 2.8 percent and France’s 3.4 percent.

Source: The Financial Times based on Bloomberg

Investors are emphasizing the scarcity of tradable bonds, leading to diminished liquidity and increased transaction expenses, constituting a negative convenience yield – a return implied by holding inventories, a persistent issue in this market. The root cause of this illiquidity lies in an issuance strategy lacking sophistication, regularity, and predictability, especially when compared to more established issuers.

Furthermore, investors point out the absence of inclusion in sovereign bond indices, crucial benchmarks for investors, narrowing the potential buyer pool. This reluctance to treat EU debt similarly to government bonds issued in their respective currencies results in a smaller, less-diversified investor base.

To tackle these challenges, the European Commission plans to boost the secondary market by introducing a repo facility and a futures market for EU bonds next year. The repo facility involves temporary lending of securities by the Commission, enhancing liquidity in EU bonds. Futures contracts, derivatives enabling investors to trade underlying securities at a future date, provide a means to hedge positions.

Additionally, the Commission aims to integrate EU debt into the mentioned indices, anticipating increased demand for EU bonds, though officials acknowledge this will require time. Repayment for NextGenerationEU begins in 2028, with member states repaying loans and grants funded through the EU budget.

In August, Johannes Hahn, the EU’s commissioner for the budget, disclosed that interest costs were expected to reach €4 billion in 2024, nearly double the earlier estimate of €2.1 billion, due to rising interest rates. To address these higher costs and other challenges, the Commission must navigate the intricate task of securing additional funding from member states during ongoing budget discussions.