A cura di Gabriele Malloggi

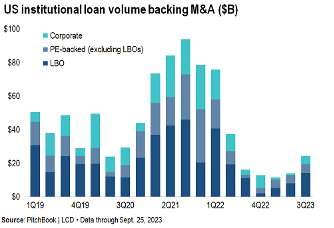

Big banks on Wall Street are refraining from participating in leveraged buyout (LBO) activities, even as the issuance of leveraged loans in the US has surged to its highest level since the Federal Reserve increased interest rates. Despite the third quarter of 2023 witnessing a robust new-issue institutional volume totaling $76 billion, major American banks are hesitating to lead the financing for risky buyouts. Their reluctance stems from concerns that these loans might end up burdening their balance sheets, a situation many of them experienced in 2022 after the Citrix-deal.

For instance, Bank of America’s involvement in buyout financings has significantly decreased this year, dropping from 71 deals in 2021 to 28 deals in 2022 and just 8 in 2023, as reported by Dealogic. This decline in buyouts by several banks highlights their apprehension due to the uncertain economic outlook, making them cautious about lending. Additionally, major banks are steering clear of deals that could result in low ratings from credit rating agencies, jeopardizing demand from significant loan buyers.

Despite this hesitation from major banks, the overall volume of leveraged loans continues to rise, driven by LBO and M&A issuances, reaching a five-quarter high of $24,5 billion. Specifically, new loans issued to support LBOs amounted to $14,2 billion, constituting nearly 60% of the total volume. This marks the third consecutive quarter of increasing supply in this category, the highest since the second quarter of 2022 when it reached $19.3 billion.

Interestingly, these rising numbers of loans are being managed directly by private credit funds, bypassing traditional banking channels. This shift has limited the options for significant lenders for major takeovers, forcing potential buyers to resort to more expensive debt provided by private credit funds managed by entities like Blackstone, Sixth Street and Blue Owl.

While it’s certainly too early to determine whether bankers have lost interest in financing high-risk debt or if they have simply chosen to abstain from the limited deals occurring this year, executives involved in buyouts, lenders from private credit firms and the banks themselves have acknowledged that conventional banks are wary of extending longer-term bridge financing without retaining the flexibility to modify terms, especially if the market experiences abrupt shifts similar to those witnessed in 2021 and 2022, following the Federal Reserve’s announcement of aggressive rate hikes.